R/Finance 2022 - Portfolio drawdown optimization with generative machine learning

R/Finance conference paper - Generating drawdown-optimal portfolios with generative AI

Published on June 03, 2022 by Emiel Lemahieu

Generative AI Market Generators Drawdowns

0 min READ

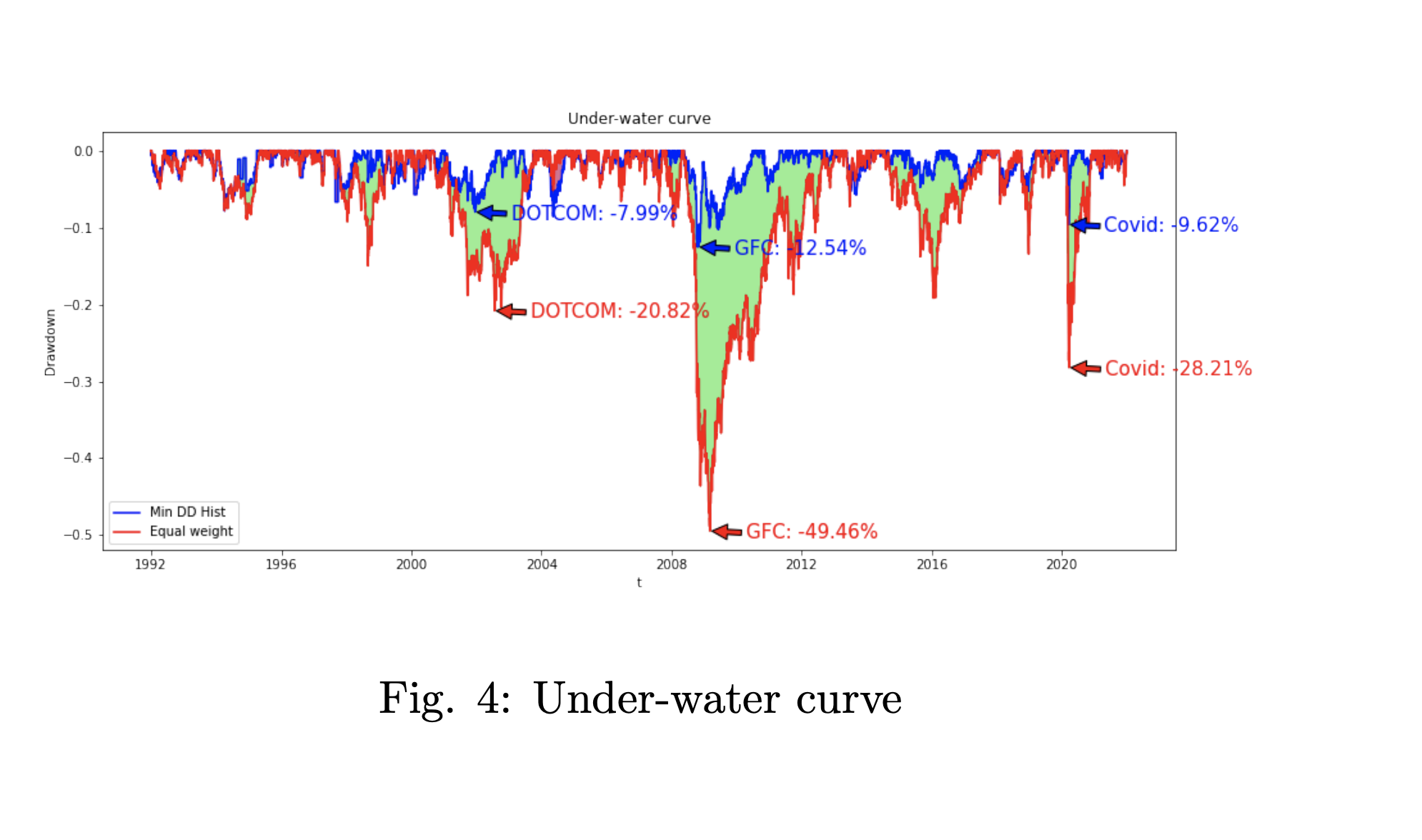

This short paper was presented at the 2022 R/Finance conference in Chicago, IL. It picks one of the above-mentioned architectures - a CVAE - and introduces a signature-based drawdown reconstruction cost loss term. The result is a host of realistic drawdown scenarios, where the optimal portfolio is defined as the ensemble expectation of min drawdown optimizers.

Preview

Download

Download the pdf below:

Portfolio drawdown optimization with generative machine learning